This is a review by our reader Satish Kumar Agarwal who recently got hands on Yes First (YF) Savings Account along with YF Mastercard World debit card.

I wanted to apply for YF range of credit cards like YF Preferred and YF Exclusive after reading their reviews and how aggressive Yes bank has become these days in launching offers. But as my city is not in their credit card serving area, I had a detailed look on their website for their other product offerings.

Yes First Savings account – Mastercard World debit card

Table of Contents

Why YF Savings Account?

After doing fair research, I zeroed in on YF savings account which comes with YF Mastercard World debit card. More so because most banks these days give same discount/ cashback for online/ offline shopping done on their Credit as well as Debit cards.

While reading YF savings account schedule of charges and benefits associated with them, I realized that most of the benefits were too good compared to those provided by other private banks for their premium savings account (Only caveat is the requirement of minimum opening cheque of 5 lacs though).

And being a YF savings ac holder, I would be one of the first beneficiary of their services like credit card, demat account etc. as and when they are available in my city.

- Requirement: 25 Lakhs NRV (they’re flexible though)

Opening Yes First Savings Account

Taking all the above things into account I decided to open a YF account and a Yes Bank executive visited my house to fill YF account opening form & fulfil KYC details and my account was live in 3 days (Yes Bank executive told me that credit card services will most likely be launched in 1st quarter of 2018-19).

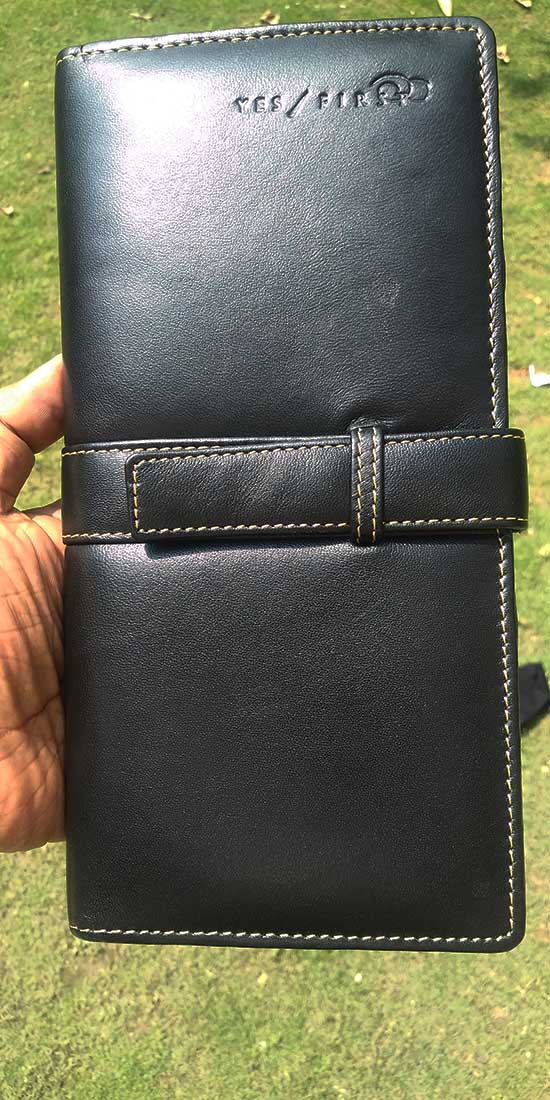

4 days (Update: it takes 12-15 days now) later I received the welcome kit containing welcome letter, MITC, schedule of charges of YF account and YF Mastercard World Debit card. The outer box was too big for the purpose (Box size identical to the size of normal cloth set box). And and voila! It also contained a beautiful Leather organizer which can keep 5 cards, a cheque book and few other papers.

Unboxing Welcome Kit

As you see in images, the debit card is beautiful n glossy with shiny texture. Its Mastercard World variant with World written above Mastercard logo in Glass type reflective texture.

Yes First Savings account – Card Holder

Yes First Savings account – Card Holder Inside

Features & Benefits of YesFirst Savings Account

General Benefits

- Mastercard World debit card comes LTF having withdrawal limit of 1 lac/day.

- Provides 3 domestic airport lounge access per quarter via Mastercard lounge access programme (Better than other Master/ Visa debit & credit cards which usually allow max 2 per quarter).

- Provides complementary Green fee waiver as well as Golf lessons at Golf courses in India via Mastercard programme, limited to 1 per month. Now this is really nice as no other bank gives this facility through debit cards AFAIK. Though their usefulness is another topic, as these kind of features are mostly provided by Super Premium credit cards.

- All sort of payment related charges (IMPS/NEFT/RTGS, Branch visit charges) are NIL.

- Cash withdrawal charges in India as well as outside India- Free. (3% Markup fee appliesthough)

- Complementary Demat account opening and Demat AMC is also NIL.

- No concept of home branch banking. Hence any branch banking at no extra cost.

- 5% savings interest upto 1 lac balance, 6% interest between 1 lac to 1 crore. Above 1 crore balance you earn 6.25% interest.

- No fuel surcharge and no minimum amount to get waiver of fuel surcharge.

Family Banking

Now the real blockbuster of YF Account: As a YF savings account holder, I can open upto 5 more YF accounts in the name of my family members (should be above 12 years) at zero balance and they will also enjoy each n every benefit of this account like me. Now this is BIGGG.

Limitations

- Requirement of minimum 5 lacs cheque to open YF account, though one can bargain and get it reduced by some margin depending upon city to city.

- Minimum requirement of 25 lacs NRV at family level (including savings balance, FD, RD, Mutual Funds, Insurance premium etc) to avoid 5 lacs balance.

- Poor RPs on debit card spends (You get 1 RP on spending Rs 200 worth 0.25 each) So effective reward rate is 0.125%.

All in all its an all rounder account that won’t leave you wanting for more. <End of Review>

Bottomline

YES Bank’s YesFirst Savings account product is certainly one the best product in the premium banking segment as this enables you to get family banking benefits with lounge access for all.

Most importantly, having YF savings account increases your chances of getting YF Preferred credit card. As Yesbank is much smaller than other banks, currently they’ve prompt service compared to rest of the industry in my experience.

However, it gets negative mark when it comes to net banking user interface, also the service may-not be that great when it comes to metro cities.

- CardExpert Rating: 3.5/5 [yasr_overall_rating]

Do you have YF Savings account and how’s the product according to you? Feel free to share your thoughts in comments below.

Got an interesting offer ( Amazon voucher) from yes bank.

“Get a complimentary voucher of INR 5000, when you meet the YES FIRST criteria and Go digital.

STEP 1

Maintain YES FIRST Program Criteria of INR 30 Lakhs Net Relationship Value or an Average Monthly Balance of 8 Lakhs of Current or Savings Account at a family level

STEP 2

Complete one digital transaction^ worth INR 1000 using YES BANK’s digital platforms (Net- Banking/YES Mobile/YES Robot/Debit Card)

I visited hdfc atm, was able to withdraw 10k 5 times, total 50k Today using my yes bank debit card.

Seems Yes Bank forgot to check their own credit score!

how many people got money stuck in yesbank?

Update: Now you can w/d funds from other ATM too. Worked for me.

Which bank’s ATM did you visit?

Which Saving is better? Kotak Bank Optima or Indus bank Exclusive?

Just stick to the mainstream banks @ Ajay Sharma especially if you are opening high NRV variant of savings account.

Why? What’s wrong with Kotak or Indusind as asked by Ajay?

Nothing. Just a matter of personal opinion. I stated what i feel, you can do what you feel

Honestly, I opened YES FIRST ACCOUNT after reading this blog spot and comments. the main intention is to get a Yes CC.

Now as I just opened yes first account last week. How many days should I should I wait to get a CC offer from them automatically if I do not do any transaction but keeping the balance in saving the account.

if it does not work like that then what is the best way to approach them?

I am a self-employed guy. so this much work is necessary because Most of the banks want salary slips /business continuation certificates/separate office address/business cards and a Company name. which was easy for me if I had these stuff. I do not have separate office name or office address, nor I have a business card.

I am a proprietor businessman, more like self-employed professional/freelancer. There is no trade name for my business. I file GST in my name only. I work from home and get money deposited to my saving account.

ITR: 24 lacs+

I mostly spend online , so a super premium card with best reward point ratio for all online transaction is best for me .

even if a CC allow wallet top ups for RP that would be great to cover my offline spends as well.

you all are credit cards enthusiasts, so I think it is best place to know if my wish to have a super premium card would be ever fulfilled.

Hope you guys recommend me so way to upgrade my credit cards.

HDFC Moneyback 5.47L – PRIME A/C – Maintaining 5+ LACs in saving account but they offer no account upgradation.

AXIS MYZONE 1.61 L – PRIME A/C – thinking to upgrade to Premium but it need to mainatain 2 lacs+ AMB .

SBI SIMPLY CLICK – Upgraded from SBI FBB card – this was taken card-on-card basis . limit is just 89000.

I have tried upgrading CL in SBI CC but I guess they never entertain CL enhancement if CC taken on the card-on-card basis . have provided my ITR and computation copy. they rejected because of some international policy.

Please suggest me which CC should I go now on card-on-card basis ?

I only have docs like POA/POI/Photos/ITR copies/ existing CC from HDFC/SBI/AXIS . can not we apply for a CC with these docs only?

regards

Askarshk

Apply via card on card basis your HDFC Moneyback cc for YFP card. If yes bank issues cards in your city then you most probably will get it. Otherwise maintain 8 lacs + in Yes First account and wait for their pre approved cc offer. It may take 3-6 months after maintaining high savings ac balance.

Hi sid !

I just opened yes first acc and they mentioned (no minimum balence required) on their websitesite . Also, Yes bank employe told me that you have to keep 5 lac in acc till the end of the opening month. After that you can withdraw it. So I want to know is there anything bank is hidding in their terms and conditions regarding minimum balance requirement and would I still be the yes first coustomer if keep 50k in acc.

Varun

As per the YES First account t&c, you have to maintain either of

1. 5 lacs in savings account balance AMB at family level (Now increased to 8 lacs recently)

2. 25 lacs NRV across products e.g. FD, RD, Insurance policies, demat holdings (Now increased to 30 lacs)

You will be Yes First customer even if you don’t maintain above criteria for some period. This period may vary from time to time depending upon banks current policy. They may choose to downgrade your account if either of the above 2 criteria not met. Though it depends completely upon bank policy.

Dear Sid

Yes First Savings account eligibility criteria recently changed upwards to 8 lacs savings account AQB or 30 lacs NRV.

I think this is mainly due to the launch of Yes Premia savings account with eligibility 2lacs AQB or 10 lacs NRV.

Under SOC they have mentioned the charge of YF World debit card as 2499/- pa, NIL for YF programme customers.

Now I suppose they will be little strict about maintaining AQB or NRV to take benefit of YES FIRST savings account via Yes First World debit card. Downgrade of YF savings account to Yes Premia or Yes Prosperity savings ac is now like hanging sword waiting to fall sometime in future ( If AQB or NRV criteria not met).

Well said n valid point.

Thank you Siddharth for your guidance.

@ Shivi

Please consider following statements before jumping to any conclusion–

1. This beautiful platform is to share and gain from each others perspective.

2. Every person opinion n experience about a product varies wildly. One may come across very

good set of people from X bank whereas another person might experience differently from

same X bank people.

3. Neither this reviewer nor anybody else can force any product to anybody. Idea is to share

knowledge thereby helping others. If anyone has better suggestions, he can always share thoughts

by sharing his experience.

4. Majority of readers/ post contributors here in this forum are well qualified to take decisions

on any credit product and these reviews only help to certain extent in making those decisions better.

At least I think in that way !!

5. Last but not the least– Constructive criticism is better but not of these kind, just for the sake

of it.

@Satish & Shivi

Lets close this conversation please. Continuing such conversations helps no one and infact distracts other readers from finding the actual answer they’re looking for.

Hi Siddharth,

Is there any other premium banking accounts which give free demat account?

Anual maintainance charge for Demate account is waived 100% in HDFC Bank’s Imperia Program,

50% waiver in Preferred program.

Thank you for the info.

@ Satish

Doesn’t make any difference now does it – whether it was 4/5 or 5/5? I just pointed out to the revised downgraded rating (and editing) after Mr. Amit (comment-34040) literally annihilated this account variant (spoken so highly of by the reviewer after deliberately withholding the most important T&C of 25 Lakh NRV) & review with his valid points.

Chapter closed 🙂

@Shivi

Ratings revised from 4/5 to 3.5/5. Please verify the same.

It was never rated 5/5.

Revised rating @ 3.5/5 from 5/5? Does it even make sense to put up this topic anymore? Might works against Yes First Savings account if not For it!

Dear Sid

Welcome after long break.

Point no. 6 under features n benefits of Yes First savings ac i.e.

Doorstep banking (1 free visit per day for cash pick up and delivery services) has been discontinued by Yes bank. On enquiring I was told that this is done as per RBI guidance/ objections. You may kindly update the post accordingly.

Also now Yes bank ac opening and receiving welcome kit is taking not less than 12-15 days. 3 of my friends have confirmed this delay in ac opening.

Alright, i’ve updated it. Its never safe to hand over cash anyways.

On the contrary, it is perfectly safe. I am an industrialist and we do cash transactions via Home banking of Kotak including deposits and withdrawal. The receipt provided by the executive is the proof of our deposit and it is always honored and same is the case with withdrawal.

Hi Sid,

Why don’t you create a what’s app group ??

Wer v can have instant discussion and also updated when a new thread is been created so that everyone could have updated info ??

Just a suggestion.

Cheers,

Kiran

I second that, with the number of user base ,a telegram channel would be much helpful

Please spare some thoughts about it sir

@ Suresh

Thanks for ur kind words.

As per my knowledge they can’t covert other yes savings ac to a Yes First savings ac. However you can open a Yes First ac separately by withdrawing money from your currently opened ac and giving a fresh cheque for the same. Better still ask the person who opened ur account.

Alternatively you can open YF1 in the name of your wife (if you are married). Once it opens, then YF2 can be opened in your name without any requirement of cheque.

Thanks Satish. I had deposited high amount and tweeted to yes bank. Based on phone number they tracked the account number and local branch manager called me about it. I feel they know about the amount there in the account. They have a form where we need to Submit it. Thats it 🙂

I am pretty much impressed with Yes Bank support. They have followed up very well.

Thanks Satish for good review. Should have read it before I opened my Yes Bank Account. I had given 5L cheque but didn’t opt for Yes First account. The main reason is I am fed up with HDFC RM’s chasing for investments. Will it be possible now to convert the account. Account was opened just 2 weeks back.

Please talk to your RM. I just got my normal yes bank SB account converted to Yes First account (whole process took about a week)

What is the point of a neutral review if the most important catch is not disclosed in an article (which any corporate hides in its products terms and conditions, and innocent customer fails to notice it, and thereafter customer is taken for a ride)

A neutral / well researched article would have mentioned the most important condition for this Yes First Savings Account i.e., maintenance of a minimum Rs. 25 lakh Net Relationship Value with Yes Bank.

If the same is not mentioned and instead, being portrayed as to ‘talk to your RM’, ‘Yes Bank won’t downgrade to maintain loyal customer base’, ‘Yes First range of credit cards will give you the Yes First savings account status’ etc., then to me it is either a major lapse on the part of the writer (which should have been corrected by acknowledging the lapse by stating the condition / eligibility criteria at the start itself) or it is a glorified attempt to market a product i.e., akin to a sales person pitching for major highlights of the product without really disclosing the catch and says ‘no worries sir, as an insider information being disclosed only to you, company has internally decided to not downgrade even if they won’t meet eligibility guidelines’ and once the customer falls for it, and then down the line, if any issue crops up, some other executive tells to the gullible customer ‘sorry sir..the term is clearly mentioned in the 10th page of the leaflet which you have signed for!’

A neutral article should have mentioned the condition first and may be later on the experts or insider tips / work around etc. If it’s the other way around, i.e., only work arounds are mentioned initially, which a sales person does to catch hold of a customer, and conditions/limitations are buried at the end of an article in a non-descript manner, which is similar to a condition hidden in a document mentioned . The aforesaid is what @Satish said ‘Please clearly read full article before concluding. Its clearly mentioned that 25 lacs nrv is one of the limitations of this programme.’

@Satish: I read your article fully. If one notices the flow of 13 paras, one would notice that initially at para 3 of the article you mentioned, that too in a bracket! ‘(Only caveat is the requirement of minimum opening cheque of 5 lacs though)’ and at para 10 second bullet point ‘Minimum requirement of 25 lacs NRV at family level (including savings balance, FD, RD, Mutual Funds, Insurance premium etc) to avoid 5 lacs balance’. The only place in your article where you mentioned about NRV, you have stated that 25 lakh NRV is required to avoid ‘5 lakh initial cheque’. My english may be poor but I do not see it as clearly mentioned that Rs. 25 lakhs is eligibility criteria / condition for having Yes First Savings Account. Eligibility criteria / conditions and limitations of a product are two different sets.

Knowledge is empowerment and this is what a forum like this should provide. I can only but wonder what harm it would have caused if the NRV criteria is clearly mentioned as the eligibility criteria! Hope one can understand my predicament of saying that this is a paid / sponsored content.

Well played!

@ Jay

Thanks a lot. Thats the point.

To make use of our resources in a better n rewarding way through this forum.

I owe a lot to this forum for the benefits I got n specially to Siddharth. Thats why I thought of sharing my experience so that everybody may benefit.

Hi Manjunath,

Sorry to say but it doesn’t work that way anymore. Or else everyone here including sid, abhishek, and also me myself would have got YFE directly.

I opened yes first account and then after few weeks the lady from chennai who was insisting me to get yes first credit card i went for it. And at that time i too said the same thing to everyone including my RM that i want YFE because it is mentioned in the welcome letter that i am eligible for YFE. But that card is exclusive and for select few and hence not issued to everyone so easily. I was issued YFP with the lowest credit limit amongst all my cards and i took up the issue to nodal officer but all i got is assurance nothing else. 😊

And my NRV with bank is quite high still this. So imagine so how strict yes bank has got in issuing cards and most importantly giving good credit limit

@ Amit

Please clearly read full article before concluding. Its clearly mentioned that 25 lacs nrv is one of the limitations of this programme.

Though its more of an income generating technique than any downgrade like thing from the bank. It serves their purpose of showing it as a super premium product as well as earn quick commission via cross selling of their products.

And please remembe this forum is to benefit from each others experience and earn money while u spend.

Dear Vinod Kannan

Its mentioned in their schedule of charges that even if u don’t maintain any balance, u will not be charged. Only thing is they may downgrade the YF ac to a normal Yes bank savings ac.

Though this also is highly unlikely as they will be losing a potential HNI. I have been told by 2 of their executives off the record that even if YF ac AMB or NRV is not maintained I will continue to enjoy all the benefits of YF Mastercard World debit card (Except its ridiculously low RPs).

@ ravi

I live in Lucknow.

I will be able to update on their banking services after some time. By then I would have got fair experience of their customer friendliness and other aspects as well.

Generally, what I look from my primary bank is most services to be available over the internet and for the rest, an RM that can assist with a runner without needing to visit the branch (unless compliance requires me to visit). My primary relationship has been with HDFC and I have a preferred account. Have seen that services depend mainly on the branch and RM. I didn’t go for a foreign bank as I thought having a wide branch network would be useful in case of unforeseen circumstances.

What primary bank are most people here using?

@ Gagan

As I don’t have any relationship with IndusInd bank, I am unable to compare between them. Also it depends upon ur personal requirements. Because if u r a frequent international traveller than ofcourse IndusInd Exclusive savings ac will have an edge due to its zero mark up fee.

Yes First is more of a lifestyle account where they frequently organize special offers n activities in branch and invite you to take part in that. Activities I have been invited in the past were related to healthcare awareness, financial awareness etc. Though I haven’t participated in any so far.

Now coming to ur query, it is safe to assume that if u open with an initial cheque of 5 lacs there is no need to maintain 25 lacs nrv. Also if ur RM says that no AMB/AQB reqd then its like modak in both hands. Having said that if u maintain a healthy nrv it may help u in some ways like easy n fast CL enhancement. If ur YFE is LTF than good, otherwise high nrv may help u to convert it to LTF. Again these all are ur personal choices. Think all the aspects n then decide which one is for u.

Any comments Sid?

You’ve said it all!

That aside, I don’t see yesbank as primary bank for day to day txn’s due to its age old netbanking interface. That being said, Indusind is relatively better. Totally depends on one’s needs!

@Satish Kumar Agarwal

Thanks for the detailed feedback. My YFE CC is LTF and so no special interest to go for YF Savings account unless it si good enough to replace one of my other accounts..

I rarely visit a branch and rely more on Netbanking etc. If their net banking systems are archaic then it’s clearly a no go for me.

@Manjunath

Thanks for the tip. I noticed YF Exclusive cc point on reading welcome letter. But I don’t think that will benefit me as Yes bank is yet to launch CC operations in my city.

One more point to add here is though my welcome letter had this point (eligible for YFE), recently they have changed this point. Now the new welcome letters say that as a YF savings ac customer you are eligible for YF range of credit cards. Sad.

If one has a Yes First Preferred Credit Card (and maybe Exclusive variant too?), (s)he can get this account with 1 lac initial deposit that can be withdrawn after account is opened & does not require any NRV. I had got this account after I got the credit card about 9 months ago because it gave lounge access to 5 additional accounts. Planning to use lounge for family members in next quarter but haven’t had any issue with NRV till now, even though I hardly maintain any.

One issue with YES Bank is – no facility to close RD online. Their Net Banking is archaic & everytime visiting branch or handing over a statement declaration to the boy who comes to pick up the RD closure letter, is a pain.

Poor bank. Despite following for 5 months (yes, five), they couldn’t credit the interest on FD. Shocking. Despite email and phone, they couldn’t show interest earned for 10k FD after it was opened and after its matured.

That’s not the big deal if they don’t credit it, but how pathetic the service is. That’s why I declined to convert yes first savings account.

It’s immature bank, I must say. Hope no one has such bad experience.

And to be frank to everybody here, I am a salaried person working for a defence psu since last 12.5 years.

@Arul

AFAIK YF debit card comes alongwith the welcome kit after YF savings ac is opened. Unsure why u had to ask for it in branch.

Maybe u escalate this to higher authorities or mail to YF customer care right away.

@ Dhruvil

Its clearly mentioned in tnc as well as website that upto 1 lac- 5%. Above 1 lacs only u get 6%.

Thanks for the information,Looks like minimum balance requirements are too high.IDFC bank offers good savings account with Visa signature card and minimum balance requirement is 25 k for full benefits.It has offers like BMS 1+1 (SIGNATURE CARD OFFER) AND 250 CB on BMS,2 lounge access per quarter,NO charges for transfers,good FD rates compared to some big banks.

This article must mention at very beginning that there is a Net Relationship Value requirement of minimum of Rs. 25 Lakh to be met within 6 months from the date of opening the account and if the TRV value is not met by the customer, then the account gets downgraded. There is a difference between minimum amount required to open an account and Net Relationship Value (which is required to be maintained across savings account, fixed deposits and other investment through the concerned bank).

Otherwise, article is more like a sponsored content from Yes Bank

yes paid article

Its not!

Hey Amit, Yes according to their terms it can be downgraded however as of now Yes Bank are not doing it. Just that the are trying to capture the mass market as much as possible.

You can also contact your RM who is personally assigned to your account and get the account charges reversed if at all charged or ask him to confirm the account variant you are into.

I don’t think it’s a paid article. Man appreciate the person who is giving you all kind of tips to make use of banking products in a wise way.

Hi!, I went for YF account at zero NRV valid for one year in June 2017. My experience with the service of YF is not at all encouraging and planning to convert this to normal SB account once the one year period is completed. RMs have limited knowledge of the products and as such not interested in active banking at all. Yes Bank is lacking on technology front and net banking is cumbersome. The irony is, it is almost one year and no official contact by a single Yes Bank executive, every time I call them and they reply! They are responsive, try to help their best but at end nothing works! In fact I opened this YF account to shift from HDFC Imperia but now I have continued with the HDFC Bank Imperia program.

Opened my Yes First account with 50000 rupees cheque and virtually maintaining Zero balance after getting Yes First Preferred Credit Card. Been 18 months now, and so far so good. No AMB Charges levied till now. Im waiting to see how long they can let this happen. I don’t know if holding on to Yes First Credit Card now gives me the Yes First Status on my savings account… Anybody there in the same club? What about u Siddharth?

Got enough cards for lounge access & BM is a call away. So I’ve no plans to upgrade to YF ac as of now, also no plans to maintain high NRV with bank for long time.

P.S. If there is a charge, you can ask RM to reverse it, which they may or may not honour. As i see that you’ve been in touch with a beautiful girl, you’ve more chances 😉

😂😂😂 Dude!!! I myself have forgotten about that Beautiful girl 😂. BTW i opened this account in Coimbatore and Now im in Chennai. So no contact with the RM.

While opening the account i was told that i would have the Yes First status for one year and within that time i have to reach the NRV required to maintain Yes First status. I did not maintain more than 20k in that account and after a year i received a mail Communication stating that if i dont maintain the required balance, my account will be downgraded. After 4 months i applied for Yes First Credit Card ( Courtesy – the beautiful girl 😁) and received it. Now im Receiving Yes First Customised mails daily. When i contacted customer care, they said that my account is still an Yes First account. So, i thought that the Yes First Preferred Card brought me back to the Yes First Status.

YFP card could be the reason. But the fact is, they wont downgrade it that easily because not many are on YF relationship and if they downgrade you, they knew that they’re loosing a potential customer who could atleast use other products like YF Credit cards to bring profits to bank.

But not everyone knew that bank is not really making profit out of many YF card holders, for now!

Yes Bank savings account have a very poor online review ratings. I was thinking of opening one, after i got the YFP Mastercard credit card. Withheld due to very very poor reviews.

What is your place of residence?

I too have this account.Opened based on my credit card relationship (I had yes first preferred that time)

I didn’t give 5L cheque, gave for 1L only

You can withdraw 1L from any bank atm /day

Doorstep banking- 1 visit free per day (Cash pick up/ delivery or any other service) is removed now

I’m YF account holder, was requested for YF debit card in branch but no response from branch. My wife got YF credit card (I also have YF credit card) after become YF account holder.

Hi,

Even for balance upto 1 lac, you earn 6% interest.

Dear Satish, Siddharth

Thanks for this article. It has come at right time – I am wondering whether to open Indus Ind Exclusive account or Yes First Savings account (already have Yes First Exclusive Credit Card).

Regarding Yes First Savings account, have a quick query – when once opens the savings account with Initial Cheque of 5 lakhs then there is no need to maintain the NRV of 25 lakhs right?

I am told that will get LTF with no AMB / AQB requirement..

Which city are you from Siddharth?

Salem.

Why don’t you consider a banking relationship with DBS Treasures? They are one of the most reliable banks out there and they are in Salem.

Have used them. Not so happy with their interface either.

Hi Sathish, one trip which you can try for Yes first exclusive credit card is, in the welcome letter of the Yes first saving account, you would notice a point mentioning that as a privileged customer you are entitled for Yes first exclusive card. So raise a request to the customer care team and mention to them that it was promised and signed by the bank head. It did work for me.

Hi Manjunath,

Sorry to say but it doesn’t work that way anymore. Or else everyone here including sid, abhishek, and also me myself would have got YFE directly.

I opened yes first account and then after few weeks the lady from chennai who was insisting me to get yes first credit card i went for it. And at that time i too said the same thing to everyone including my RM that i want YFE because it is mentioned in the welcome letter that i am eligible for YFE. But that card is exclusive and for select few and hence not issued to everyone so easily. I was issued YFP with the lowest credit limit amongst all my cards and i took up the issue to nodal officer but all i got is assurance nothing else. 😊

And my NRV with bank is quite high still this. So imagine so how strict yes bank has got in issuing cards and most importantly giving good credit limit.