The best way to find the cards that I hold is to have a quick look at the best credit cards article. If you are reading Cardexpert for sometime, you might be aware that I’m currently holding 10+ active credit cards and you might be wondering why the hell (or heaven for that matter) I’m holding so many cards.

No, it’s not because I’ve unlimited spends, but because of these 5 reasons that I felt you should know too,

Table of Contents

1. I love the Design

I’ve good history of getting cards that look amazing and not rewarding. For ex. Axis Select card. It looks so beautiful that I try to find a value out of it just to get it.

Sometimes I get them even if I don’t find any value. I’m happy to pay for the design!

It may sound stupid for some of-course and that’s totally fine. Everyone has their own interest towards things in this human life and I’ve silly some.

I’ve over 200+ cards (credit/debit/prepaid) in the collection accumulated in the past decade or so and it’s fun to look back at the beautiful designs once in a while.

2. Attractive Sign-up offers

I might have received an attractive sign-up/upgrade offer but it’s not published publicly.

You would know it most of the time but at times I may not even mention this, as the offer maybe short-lived and if such offers are published publicly it may be taken down as soon as the article goes live, as our fellow readers from banks are also reading the articles.

This happens because banks send lucrative offers like additional points offer with upgrade, FYF or LTF cards based on premium profiles but when this is out in public domain, customers start to bombard the bank with queries, which will eventually make them to get rid of the offer.

Hence, to save everyone’s time, I don’t publish them.

I might have closed a XYZ card and publish that here but I may still have access to it someway or other, like, getting that card for one of my family member so that I can continue to access the benefits through them.

While I’ve mentioned it here and there before, I may not mention it every-time.

Not just the card, even the reward rate may differ, as many of you might know that now as well.

These things are not spoken about in public for obvious reasons. I see more such sweet spots coming up often these days but are not written here, as they may vanish in no time if done so.

4. I keep changing cards

I’m frequently asked “what cards you’re currently using?”

The reason why I don’t cover it is because I keep changing the cards very often, like every month or two and unfortunately I may not be able to update that article very frequently to make it relevant.

While I may keep changing the cards, I continue to have only two or three cards in my wallet almost all through the year.

5. It’s an experience

To evolve as a human being, one has to upgrade to better/finer experiences in life. Enjoying 5X/10X rewards alone is of no use.

Enhancing many aspects of our life through rewards is generally cheaper than spending out of pocket. So even the expensive cards are cheaper in that angle.

While that’s on one side, sometimes I get a card just to experience the product, even if its not so good. For ex, the recently acquired Kotak cards (White card & Privy League card) hardly saw any spends so far, but I got it just to experience Kotak credit card services.

Sharing these good/bad experiences not only helps me and you, but also banks to fine tune their products. It’s a triple shot. So why not!

Bottom line

To sum up, I want to convey that there are always few things beyond the content of a typical article and you’re not given the whole picture through my articles intentionally as they’re free and open to everyone.

This holds true not only for Cardexpert but for almost every blog in every industry, the % of info might vary of-course.

This is because when everyone knows everything, the % of misuse goes up and so it no longer remains the way it is. So it eventually speeds up the devaluation.

So blindly getting the cards that I get may not be financially good to you.

Hence, You’ll need to do the math and then decide for yourself.

Having said that, the articles are usually equipped with necessary information and reasoning for you to decide. And not to mention, comments are always there to help, thanks to the contributors.

So what can you do to maximize credit cards at its best? Well, you may read the articles, probably once or twice a month, connect the dots and get to know the sweet spots yourself.

This works for most, unless you’re on high value spends of >20L p.a., in which case One-on-One paid consultation may help to access all the content in its totality.

Either way, plan your own strategy. Someone saying you can get 10% reward rate on an unrelated benefit for your life is 0% useful for your life.

Follow none.

Hence neither follow my portfolio of cards, nor anyone’s. Only you know what card you need to enhance the lifestyle you’re currently living.

Good One Siddharth,

But I think what you said here should be obvious to all. Different people have different needs. Be it investment, life goals and CC. As a content writer you can provide the best available options and it is user’s discretion to choose if it is okay for him/her based on their lifestyle.

I learned it hardway after applying and receiving some cards that I don’t know what to do with now 😀. Nowadays I put SIs (recharge, small insurance) of my regular payments to those cards and auto pay via bank just to keep them alive. May be you can write something on how to keep multiple cards alive OR how to systematically close them 😬.

And about the offers, yes that also correct. As more people know it, less lives the offer. That is why banks profile the customers and send different offers. Though I am sure you will post the offers that will not hurt the system.

Sorry to say Sid but i don’t agree for point no 2. I believe you always post whatever you are aware of. You should think of your readers and not for banks even the offers are short-lived. You shouldn’t care for banks. I really have full trust on your post and they are really helpful. Please keep posting

Not just the card, even the reward rate may differ, as many of you might know that now as well.

Lol did I understand it right? Did you mean for same card and same spend category, someone may get 1% points and some other may get 2%? Never heard of this.

Don’t worry about that as better reward rate is expected in a month instead.

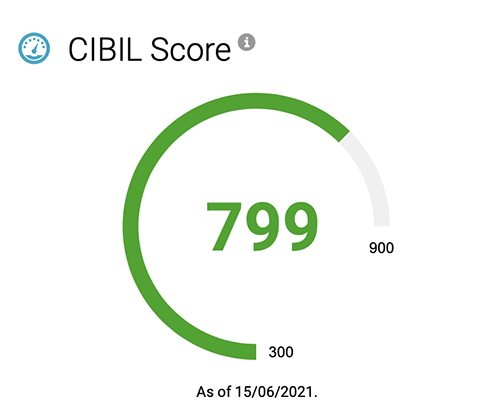

200+ cards in a decade !! And your credit score is still hot enough for new super premium cards? I thought that gets affected with more new cards or more old closures.

Yes, it is. Have a look:

how does it not effect your credit score

I guess the active/actual credit cards might not be more than 50 -60 ?

We have around 15-20 Banks issuing credit cards, suppose 3 from each bank makes the count 60. (Considering personal cards only).

I’ve started my journey of credit cards 4 years back and I go with max 1-2 cards per quarter . Now Im holding 23 cards from 15 issuers. My Score is still 810+.

Which are the 15 issuers?

@Sid really like what you said here while I agree with most of it but I have a question on why you don’t share the CLs for the cards. For example I was told by a SBI manager that Aurum can only come with 10+ lac limit and my current humble SimplySAVE had only 4-5lac limit so I dropped the idea.

It was much later that I found out it’s not so and that 10+ CL for Aurum is not a thing at all and this info restarted my Aurum cravings.

Secondly do share C2C based cards it’s often that I see in the market that people actively discourage C2C based applications such as in the case of BoB Eterna. I was told that I would get a max limit of 2lac on C2C no matter which other card I hold with what ever limit but that was not the case since I got a 6-7 Lac limit but had to downgrade it since points were not being issued for spends. BoB had the audacity to take all my paperwork “ITR/Payslip and issue an Easy card 😛

Point noted. Thanks.

Sad to hear about Aurum. You could have asked here, our friends here happy to help. Aurum issuance is relaxed only since past few months anyway.

Sales / Field guys in any bank generally do-not know anything about Credit limits and how it works. They get to a conclusion based on the profiles they handle, in BOB case, they usually handle beginners and so the assumption about low limit.

Hi, I have been holding an Amex platinum charge card. Would like to have aurum card in my wallet because it comes with visa or master. Which I can use, where Amex is not being accepted. However I don’t have any relation with sbi cards and bank. Can you please help me with the process of getting one ?

SBI Aurum is an under performing card. Any decent card with 3-5L limit can get you an Aurum card with the help of an Aurum RM. I myself got one that way, as I closed my Elite much earlier. Don’t do the same mistake even if you don’t want SimplySave. Just get hold of an Aurum RM, get it done on c2c. Then if you want to close simply save, just transfer the limit to Aurum and close it. Voila! Free LE 😉

But SBI splits the existing limit. I tried twice and same happened both the time. I declined as I don’t want to split.

Aurum requirement is only around 2.5L limit in existing card.

C2C around 4L is sufficient.

***

Exactly. Everyone’s travel habits, choices are very different and there are very few cards which suits all..

Some like pure no nonsense cashback, some vue rewards and some value experience