HDFC Bank has recently announced new minimum requirements for existing Infinia Credit Card cardholders. Infinia is the bank’s evergreen flagship super-premium credit card, one that has long served as inspiration for competitors.

If you hold HDFC Infinia, you’ll now need to either spend or maintain a certain amount with the bank each year or risk losing the card.

Table of Contents

New Requirements

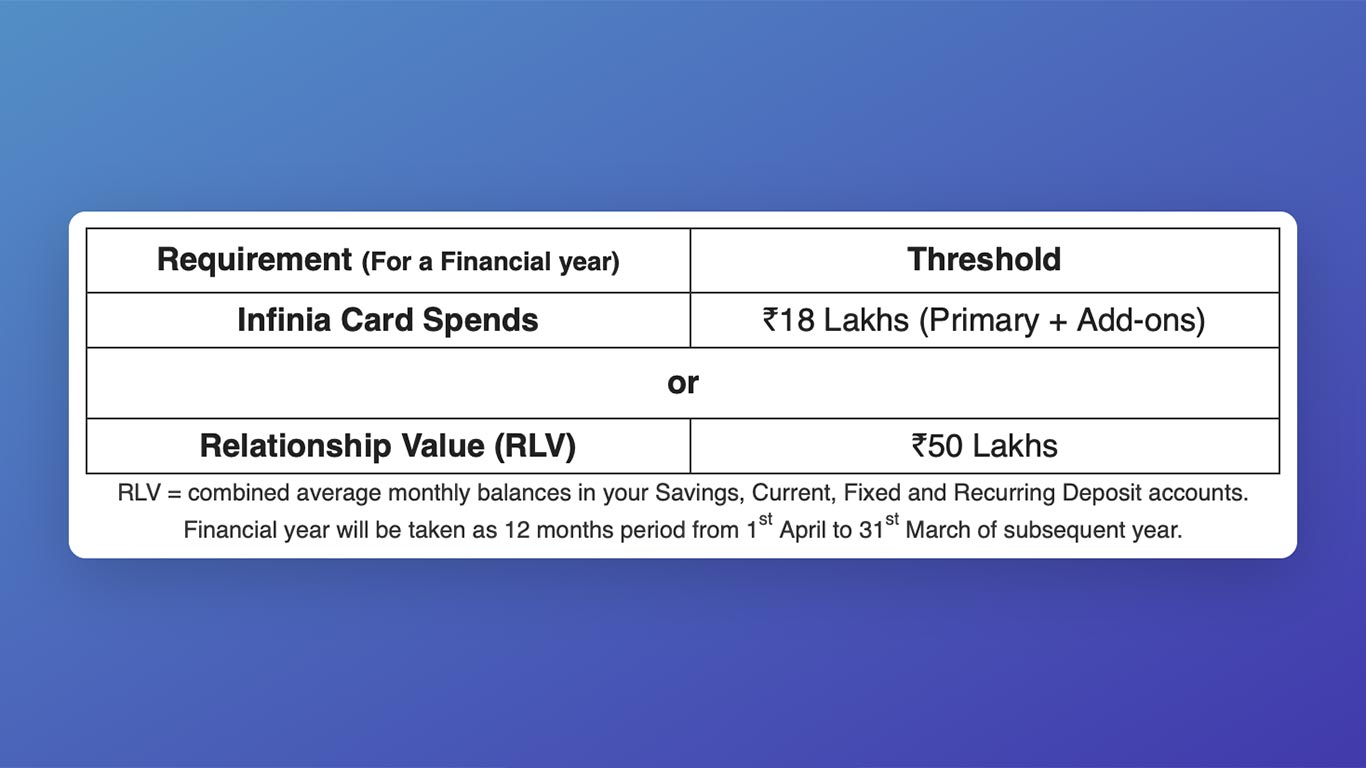

Starting April 1, 2026, Infinia cardholders must meet at least one of the following each financial year to retain the card:

- Spend ₹18 lakhs on the Infinia card between April 1, 2026 and March 31, 2027, or

- Maintain a Relationship Value of ₹50 lakhs (savings, current, and fixed/recurring deposits combined) with HDFC Bank during the same period.

Those who don’t meet either condition will be notified in 2027 and may be downgraded to another card or removed from the programme altogether.

Additionally, some cardholders were asked for a ₹3 lakh spend requirement within 2 months to hold the card before the new financial year kicks in, these were likely accounts with low spends and low relationship value.

Why Is This Happening?

Over time, many Infinia holders stopped using it as their primary card, keeping it purely for status, lounge access, and SmartBuy perks while routing everyday spends to higher-rewarding cards like the Axis Magnus Burgundy.

On top of that, a large number of cardholders got access to Infinia in the recent years without truly meeting the eligibility criteria. This gradually diluted the card’s exclusivity.

HDFC Bank now needs to clean up the portfolio, even if it means some genuine cardholders get caught in the crossfire, since pulling spends back from other rewarding cards is no small ask.

My Thoughts

This is a good move. A criteria-based trim is far better than an product devaluation, and the bank has given cardholders a full financial year to plan ahead. So only serious cardholders can keep Infinia going forward, just how it used to be pre-covid.

That said, if the bar is this high, the benefits should reflect it.

Super Premium Credit Cards with similar relationship requirements like the HSBC Premier offer perks like a 1:1 points transfer ratio and complimentary airport transfers.

So if HDFC Bank is asking cardholders to commit at this level, it’s fair to expect a refresh in return: better benefits, with possibly a higher annual fee so that it can sustain for a longer period.

My bet is that an upgraded Infinia with stronger perks is on the way, and if so, it remains one of the best cards to hold.

This change also probably means the much-rumoured Infinia Reserve can’t be expected anytime soon, the bank likely wants to stabilise the existing Infinia base before launching something even more exclusive.

Bottomline

HDFC Bank has made it clear, you can’t just hold the Infinia card without actually using it. From April 2026, you need to either spend ₹18 lakhs a year on it or keep ₹50 lakhs with the bank. If you don’t, the card will be taken away in 2027.

If you’re already spending big on Infinia, nothing changes for you.

But if you’ve been splitting spends across multiple cards and barely swiping Infinia, now is the time to decide: do you want to make it your main card, or let it go?

The bank has given us a full year to figure it out. That’s fair isn’t it? what do you think?

Didn got any confirmation about continuation of card 😱

Did you all got the confirmation ?

No communication till now.

Neither for those who can continue nor for those who didn’t achieve 3.0 L spends in the 2 months window.

VIKRAM has received as per the his comment.

I received my confirmation around end of April that card will continue till March 2027.

I am interested in the other way round: people who did not meet the milestone, did they get any notification about card not continuing? And what is HDFC offering as replacement?

Looks like they have quietly removed pharmeasy from 10X in shopping starting May.

Today got a continuation email confirming that I have reached the spend threshold for this year and that I can keep the card till 2027 and the next review on whether I can keep the card past that will be in April 2027.

So is it financial year that they are calculating then? Because my card membership year is December to November only.

Typically, HDFC Bank’s historical playbook has been to dilute the existing product for low value cardholders, while upgrading a fraction to a new tier. If they’re not doing that here, they probably intend to keep Infinia as the top tier for now and not introduce Infinia Reserve yet (if at all).

These are usually the consequences of business teams’ sins running promos that were never healthy in the long term.

The more I ask around, the more this looks like a big goof up by HDFC. I hear almost every one getting email that they have only spent about 11L so far and they have to spend another 3L in March and April. If you are wondering what the goof here is, it is the fact that this calculation of 11L spends seems to be just a random number. Because many say they spent more than that and some agree they never ever spent that much in a year ever.

Not sure what to make of that. Did they send the template as it is to everyone without substituting the real values for each customer?

They took the values until December I suppose and that might have caused the confusion.

Is it? But nowhere is it mentioned. In fact even for me they said I will have to spend 18L in a year and the next evaluation will be in April 2027 to see if I will get to keep the card for the upcoming year or now. That only made me feel that they were talking about the financial year.

I’m referring to the email, that read something like:

“Your Current Standing*:

Cumulative Infinia Card Spends from April – Dec 2025: ***”

To be honest this is pure blackmail. At the time of card issuing they never said anything like this right. what about people who just paid annual fees. I request all infinia holders to not take it for granted and report to RBI. I bet this would be revoked immediately by bank.

I did same in year 2016 and bank did everthing to comfort me.

It is bank mistake to give card to all.

I got emerald plastic but going to ask for metal. And now i am very Happy with my DCB plastic. Got upgrade for Metal but i did not take.

Irrespective of what HDFC Bank claims, can they legally revoke an LTF card or downgrade it without explicit user consent?

There’s also a broader question—has any issuer done this before with credit cards?

LTF cardholders would be wise to ignore such communications and avoid inadvertently clicking on any “I agree” links that could be construed as consent.

They have the right to revoke a card but can’t provide another card without consent. But this is where they are clever. If the user refuses to accept a downgrade, they stand to lose the reward points. Because then it will be purely a cancellation of the card and so the user will lose the reward points altogether.

What will happen to biz black card , if infinia will be downgraded….?

If i pay tax to reach 18lac mark, will that be counted?

Yes, there are no exclusions for 18L spend criteria.

Even wallet load or jewellery expenses?

I am someone who spends about 12-13 lakh a year and did my maths that even spending 18 lakhs a year is worth it as I get almost 2 lakh from this card every year (mainly via 10x on pharmeasy, Amazon vocher, shopping vocher). I have moved some of my internet banking payments (school fees) to card for which I am incurring additional charges but all in all spending 18 lakh to get back 2 lakh by spending additional 5-6k in charges makes sense.

If you are already having that much expenses to be made then it’s definitely worth to do that.

But not for someone if the max expenses on his/ her Credit card is in the range of 12-13 lakhs and need to spend more just to reach the 18.0 mark.

I am in for this. Its good that Spend based criteria is introduced, this will lead to a stable product with no devaluations. We already say cap for Amazon increased for 20K for sometime and unlimited cap for myntra and Swiggy. Though they need to improve transfer partner ratios and monthly cap for points.

“The DCC markup fee will be revised to 1.75% on each international transaction carried out in Indian currency (INR) at an international location, or transactions carried out in INR with merchants located in India but registered in a foreign nation”.

Received the above message today for Infinia cards

From 15th May, 2026

1. DCC mark up fee will be revised to 1.75%

2. In the event of lost, stolen, or damaged card, the re-issuance fee will be:

₹ 3,500 for Metal cards

₹ 199 for Non metal cards

what happens to the cardholders who got LTF infina when the corona time.. Are they also comes under this 18 L category

Yes, for everyone.

I have this card issued in 2016. I didn’t receive any email. i specifically called customer service and they told there is no email sent for my account and there is no 18 lakh spend requirement for me.

Has the transfer of DINERS BLACK points to airline partners under a different name been halted?

> On top of that, a large number of cardholders got access to Infinia in the recent years without truly meeting the eligibility criteria. This gradually diluted the card’s exclusivity.

They gave it to me, of their own volition, lifetime free, during COVID. I didn’t ask for it. They gave an offer, I accepted. No RMs were involved. My spends were not much, barely 3 LPA on a Moneyback. The dilution bit is almost entirely their fault.

> My bet is that an upgraded Infinia with stronger perks is on the way

My bet is that _nothing_ is coming, Infinia will remain the same or get devalued. Because the competition is doing the same thing with their super-premium cards.

Banks have stopped showering their card blessings. It’s time to move on to simpler cards and fewer spending.

> If you don’t, the card will be taken away in 2027.

We’ll cross the bridge when we get there.

In my own personal experience, things are not in black and white like this Let me explain, from what info I have gathered.

1) Most people who have received this enforcement notification have been ones that have already spent 10L+ on their card to ward off the annual fees. Some of those have been asked to spend 3L in March and April while I have been asked to spend 2L because this is my primary card and my spend is already comparatively high.

2) I know people who have horrible limits for Infinia and some who have spent under 5L, no other relationship with the bank, and still haven’t received this email. Now, I can’s say if this is because the bank has already decided these people can no longer be Infinia customers. But even then I would feel it as essential for the bank to communicate. Most banks will. HDFC may not, given their history.

3) I know a few people who were forcibly given this card without even asking for it. Yes, that’s right. Given by recommendation/insistence by branch managers. Some of these are strictly against credit card usage. Some don’t even know where their card is. 0 transactions in years. They didn’t receive this email either. I would like to assume that their card account must have gotten closed already as I think the card gets activated only upon first usage. But these people still receive offer emails for their card. As strange as it may sound, this is true.

I can’t see this as the right move. If you want to keep a card exclusive, you keep it that way from the beginning. If you let that slip, then you introduce a new card that is above your current top offering. This will help them in that some card freaks would wanna become eligible for the card and will go on a spending spree. But giving something and then taking it back with this kind of email, it is very poor customer service.

Just think of this. You have to spend just 10L to avoid annual fees. And then 18L to keep the card? What sense does this make? The person who proposed such an idea should have a sanity test done on himself. But this makes me wonder if the bank is okay with people spending under 10L and paying the annual fees and is only upset with people spending 10L and avoiding it? I feel like there is a strong possibility for this. If so, then why not just increase the spend threshold for the annual fee reversal itself?

I feel like becoming the top dog has somehow gone to their heads. My recent interactions with their Infinia Priority Customer Care has left me wanting. I have always had mixed feelings about HDFC. They are the least transparent in most aspects. I have had many tussles with them regarding rewards points. One of the main reasons I have stuck to them is that I have been their customer from 2010. I have never been a customer for any other private sector bank for this long. And it is also my oldest card relationship currently. But if they think they are so royal and I don’t deserve to be their customer, then I don’t honestly want them anymore either.

They had set me just 2L to spend for March and April. It is very easy for me to reach it. But I am not doing it. I am not doing it on purpose. If they think they are doing me a favour by letting me be their customer, they can go to hell.

You are first person I came across, who got a mail for 2L spend for March April. Most of them receiving similar mails were asked to spend 3L including me.

We will come to know the truth wrt other things in future only.

I feel like it is probably because my spend is higher than most others who got this email. But I can only assume so. Do you know anyone who has not even reached 10L on their card till Feb 2026 still getting this email?

No, I don’t know anyone like that but I too would like to know if someone can share their experience.

My spends were 11+ for that period but in the mail it was written 8.5 only but I didn’t contest for that as it was much lower from what they were asking for.

I have spent 13.27 lakhs, as per their email and yet I am being asked for 3 lakh in 2 months. I have a vacation planned so it won’t be difficult, but this is unfair to ask to reach almost 18 lakh without prior notice and it’s difficult with the meager 7 lakh limit. I use it as primary but to avoid too much credit usage I routed almost 11 lakh just 3 months ago to my axis atlas.

If you consistently reach 20% of your limit on any card, it would impact your credit score. So, please don’t fall into the trap of trying to impress HDFC by compromising your credit score.

What I find seriously ridiculous about HDFC’s ask is that, this card though is claimed as invite only, it can be applied for by anyone with a monthly take home salary of 3L. If they expect us to spend 18L a year, that is 1.5L per month and that is 50% of your take home. Can you imagine what that will do to one’s credit score? HDFC never operated on any logic and now they seem to have completely lost it.

The monthly take home requirement is 5 lakh now

Got the same message.

I can touch 3L in this month. Mostly manufacturered.

So will qualify for another year. Where I am sure I will touch 18L.

In that scenario, mostly likely downgraded to which card?

May be to Regalia Gold as Infinia is on the Visa / Mastercard line.

No information till now.

Will come to know in May if HDFC actually downgrades someone.

That is exactly why it sounds so ridiculous in the first place. In the HDFC cards ladder, immediate below is DCB but that has acceptance issues. But if you downgrade someone to Regalia Gold, someone who was worth an Infinia till now, imagine how that would be? I mean if we think Infinia is diluted during Covid, Regalia has never been exclusive at all. Not talking only about Regalia Gold here, any variant. You don’t even need a take home of 1L for getting the Regalia. And that requires only 4L spends to ward off annual fees. So, people who have spent upwards of 10L so far, are suddenly going to be downgraded to Regalia Gold, which is already the card almost anyone can hold.

Any bank with an ounce of common sense won’t do that. But HDFC is very much capable of doing it. Let’s see. I am hoping I at least get the DCB, so I can find a backup card or just manage with whatever I already have.

But then, I can’t not think that this maybe a ploy to simply wipe out all rewards earned. I mean if they give me a Regalia Gold then I would reject it. And that would mean I lose all the points. I have not been able to use reward points effective since the pandemic as travel almost came to a halt. I let points pile up, only redeeming if something is expiring. But since I got this email, I have been trying to redeem it as much as I can, so I don’t suddenly lose them all.

HI Vikram,

I am a user of Diners & started with Diners Rewards, then Premium, Privilege, Club Miles & now DCB PVC using it from 2016. There was a time when Diners had acceptance issues like Amex. But they have worked hard on it. I hardly faced any issues using it. Though I always keep Visa/Master card along but the transactions always went through. Any POS terminal with JCB/Rupay card accepts Diners card. Instead Amex is still far behind than Diners platform. You can take Diners card and no need to carry an additional priority pass for airports. It works seamless. If they give that option, you can give a try, use it and anyways your points will be transferred to DCB to 1:1, if you still find issues, redeem points and close it or move to some other variant.

Thank you buddy. It has improved but some shops here in Chennai at least, still don’t take it or ask for 2% extra. Surprisingly even some shops in big malls don’t take that. Anyway I think I can manage with a DCB. I have enough backup cards to start with. If I see issues with using the DCB, then I will indeed go for another backup card, that is if I have to make a lot of expenses on that card.

Hi Sid,

Any info on exclusions? Like Fuel, insurance, rent, Govt payments etc…

Nothing excluded AFAIK, so all spends should ideally count.

While I understand that the information about charges on a statement may be redundant for most Infinia holders (& cardexpert readers), respectfully, it may be helpful for those who need absolute clarity. (I was asked the same specifically by a UHNI Infinia holder)(hence my post)

The spend requirement of 18 lakhs does not mean that the total of 12 statements in the FY must be equal to or more than 18 lakhs; it only refers to the total retail spend, so, in essence, it is exclusive of …

All charges and taxes, such as DCC/forex cash withdrawal/finance/overlimit card replacement/reissue, fuel surcharge, and conv-fee on rent/utilities/3rd party wallets, if applicable, processing/foreclosure fee(s), balance transfers and interest, with corresponding GST on all of the above, are excluded.

Also, even retail transactions done on EMI are excluded.

No EMI spends (only principal amount or otherwise as a whole), regardless of direct merchant/HDFC/Smart Buy pre/post transaction or OTP page conversion online/offline, including jumbo and Smart EMI, etc., will be considered in the new 26-27 FY Rs 18 lakh milestone/target/requirement for Infinia.

Only full-swipe single transactions (both offline and online) (primary plus add-ons) will be counted. No MCCs are excluded otherwise.

All reward point earning and applicable caps are on an as-is basis.

Example: Single-swipe tax or government transactions will not fetch reward points as Bizblack does, but will be counted as spend.

Unlike other banks, Transaction(s) value(s) exceeding the given credit limit are allowed (by paying the current balance in a single statement multiple times, or those done within approval within a temporary limit enhancement at HDFC’s discretion) and will be counted. However, the fair usage policy for reward points applies.

Voluntary Infinia downgrade or closure will not affect biz black or other super premium floater cards, as previously communicated (revoked sometime in the last week of March)

Spend, or TRV, respectively, is applicable to all Infinia holders individually, regardless of whether the card is Paid or LTF, Metal or PVC or if they are part of the family banking program

LTF holders can keep the card for free as long as the TRV is maintained in the customer ID linked to both Infinia and the individual account(s).

Although my own TRV was a few times the current Infinia requirement, as the primary account for the Imperia family banking, my dad’s TRV, as an LTF Infinia holder for his rarely used individual savings only, was in the thousands

There is no change to the card membership year. The card membership year and the FY spend requirement are also mutually exclusive.

Both will have to be met separately

Most cardholders will have overlapping time frames, and an 18 lakh spend will overshadow the 8/10 lakh fee waiver for paid cards

For those who don’t, it’s sorry for the inconvenience as of now

Also, personally, especially in my circle, it is not only low spenders. Some Infinia holders who have met the TRV and/or the spend condition or both, have been asked to spend an additional 3 lakhs

while some who haven’t used their card in ages or don’t even have HDFC accounts, let alone any meaningful TRV, have not been asked anything

This information about EMI exclusion as is specifically confirmed by a senior supervisor in Infinia/Imperia phone banking, by direct confirmation from the Infinia product manager, and by my RM, who was CC’d on the email, as written proof.

PS (touchwood) never used the below option, so did not ask and thus cannot confirm the same.

The above information is true to the balance being paid in full for every statement(TAD), so it is unknown whether the above EMI rule applies only to transactions incurred or is a blanket rule encompassing the MAD and TAD of the statement due as well (best example: AMEX Charge cards).

As in, whether the spend will be counted or excluded as a whole for the statement, in case the Infinia member makes one shot transactions but chooses to pay only the minimum due and roll over the remaining statement balance over on a deferred basis to subsequent statements.

Hope this helps !!

Thanks for unwrapping the fine print, Vivek. Glad to see you here, been a while. 🙂

Wow! That is a lot. But none of this was communicated by the bank to us I guess.

My card membership year ends in November. So, I have no idea how they calculated the spends and said I am falling short. Because if they only accounted for November or December to Feb, then I would have been severely short. If I calculate the card membership year, it comes well above what they claim I had spent. So, only HDFC will know what period they are talking about and how they have arrived at that number.

Does NPS contribution will lead to Milestone consideration of 18 lakhs? Any other inclusion or exclusion?

🙏

No exclusions has been mentioned in the mails. Not to anyone from the known souces.