The Axis Bank Magnus Burgundy Credit Card (or Magnus for Burgundy) was launched following a significant devaluation of the regular Magnus Credit Card. The Magnus Burgundy Credit Card is exclusively issued to the bank’s true Burgundy customers and is ideally suited for those with high spending pattern.

The Axis Magnus Burgundy Credit Card is not only the best credit card in India for HNI’s but also the best in the world because of it’s lucrative reward structure on ongoing spends. Let’s see how it stands in 2025,

Table of Contents

Overview

| Type | HNI Credit Card |

| Reward Rate | 4.8% to 25% |

| Annual Fee | 30,000+GST |

| Best for | High Value Spends |

| USP | Airline/hotel transfer partners |

Due to the high joining fee, the Magnus Burgundy Credit Card is specifically designed for high-value spenders who are willing to invest some time to explore its airline and hotel transfer partners to maximize the point value.

Fees

| Joining Fee | 30,000 INR+GST |

| Welcome Benefit | 5,000 INR Yatra Voucher |

| Renewal Fee | 30,000 INR+GST |

| Renewal Benefit | Nil |

| Renewal Fee waiver | On spending >30 lakhs |

- Spend requirement for annual/renewal fee waiver will exclude spends done on: Insurance, Gold & Fuel

It’s funny when you get only 5K INR voucher while the joining fee is ~35K INR (with GST).

But if you know the value of airmiles or hotel loyalty points, you would close your eyes and go for it.

Design

The Axis Bank Magnus Burgundy Credit Card comes in a light-weight metal form factor and primarily operates on the Mastercard platform.

Interestingly, the bank has chosen not to include the word “Burgundy” anywhere on the card’s design.

As a result, it’s impossible to differentiate between the regular Magnus and the Magnus Burgundy solely based on appearance.

Rewards

| SPEND TYPE | REWARDS | REWARD RATE (EDGE REWARDS PORTAL) | REWARD RATE (POINTS TRANSFER at 5:4) |

|---|---|---|---|

| Regular Spend | 12 RP / 200 INR | 1.2% | 4.8% |

| Axis Travel Edge Portal (5X) | 60 RP / 200 INR | 6% | 24% |

The earn rate of Edge Rewards on regular Magnus & Magnus for Burgundy are same, however, because of the difference in points transfer ratio (5:2 for Magnus / 5:4 for Magnus Burgundy), it makes a world of difference, like 100% more value to be precise.

Exclusions for Rewards:

- Rent (Capped at 50K INR a month)

- Wallet, Utilities & Gov. Spends

- Insurance, Gold/Jewellery

- Fuel

Accelerated Rewards

- On Spends of >1.5L a month: Get 35 points / 200 INR (~14%)

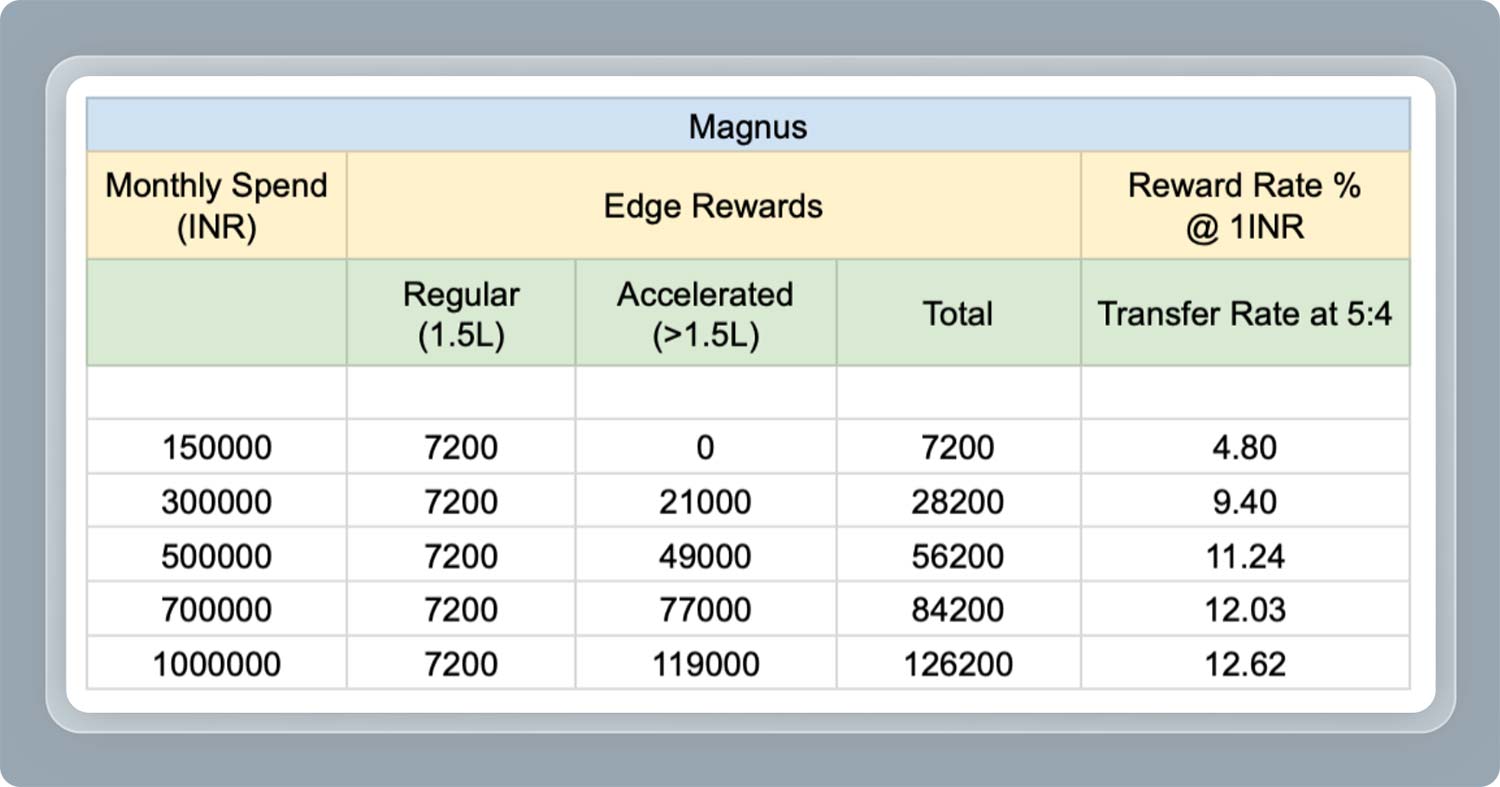

Magnus Burgundy is an amazing credit card for high spenders as its reward rate beats any card in any bank in the “world”, especially when “monthly” spends go up.

You get 14% return for spends over 1.5L INR in a month. But realistically, here’s how the numbers look like on average, as first 1.5L spend gives only 4.8% return.

As you can see, ~3L monthly spend on an average is the sweet spot to get close to 10% reward rate.

To give a perspective of how lucrative it is, HDFC Infinia used to offer the highest reward rate for very many years, which is 3.3% on regular spends.

On top of that, if you move the points to Accor, then it’s 1.8X the value, which is a sweet 18% return on day-to-spends.

5X on Travel Edge

- Earn 60 points / 200 INR (~24% as miles) upto 2L spends a month

- Earn 35 points / 200 INR (~14% as miles) beyond 2L spends a month

While 5X Rewards on Edge Rewards is good in a way, do note that dealing with Travel Edge portal is not an easy affair.

While 5X on travel edge is good, especially for flights, HDFC Infinia gives 33% return on smartbuy hotel bookings.

Redemption

- Redeem Edge Rewards to points/miles at 5:4 ratio

- Max up-to 10L points a calendar Year: 2L to Group A & 8L to Group B

| GROUP A | GROUP B |

|---|---|

| Accor (Hotels) | ITC (Hotels) |

| Marriott (Hotels) | IHG (Hotels) |

| Wyndham (Hotels) | Qantas Airways |

| Air Canada | Air India |

| Qatar Airways | Air France |

| United Airlines | Spice Jet |

| Singapore Airlines | Air Asia |

| Turkish Airlines | |

| Thai Airways | |

| Japan Airlines | |

| Ethiopian Airlines | |

| Etihad Airways |

If you’re wondering where to redeem, Accor Hotels (1.8 INR per Accor ALL Point) in Group A & ITC (1 INR per ITC Green point) in Group B are the safe & popular partners.

If you’re looking for airline partners, Air Canada, Singapore Airlines and Qatar are the next best.

But be aware that airline partners are risky as they tend to devalue miles overnight and you might end up sitting on ~50% lower value, just like how I’m sitting on few lakh miles with United Airlines.

Airport Lounge Access

| ACCESS TYPE | VIA | LIMIT | GUEST ACCESS |

|---|---|---|---|

| Domestic Lounge Access | Visa / Mastercard | Unlimited | 4 |

| International Lounge Access (Primary) | Priority Pass | Unlimited | 4 |

Guest access is a good one to have and it is limited to 4 per “calendar year” which is decent but 8 as before would have been lot better.

Note: With effect from 1st May 2024, the airport lounge benefits (domestic only) are available after spending 50K INR in the past 3 calendar months. This is cruel for a card of this grade.

Airport Meet & Greet

- Complimentary Access: 4 / Calendar year

The domestic airport meet & greet service – which Axis Bank calls as “airport concierge” service is the USP of this product. It gives VIP Assistance Services for a smooth and hassle-free airport transfers in India.

Add-On Cards

Getting add-on cards with any Axis Bank credit card is tricky but is getting better.

I wouldn’t suggest taking add-on cards if you’re looking for peace of mind. Because even if you get it, you might end up in OTP handling issues. Hope Axis Bank fixes this Add-on cards issue forever.

Forex Markup Fee

- Foreign Currency Markup Fee: 2%+GST = 2.4%

- Net Return: Rewards – Markup Fee = 4.8% – 2.4% = ~2.4%

2.4% gain on forex spends is a very good return on spend in the industry. On top of it, if your monthly spends are higher, then it’s undoubtedly the best credit card for forex spends.

Features & Benefits

- No Cash Withdrawal fee (but finance charges applies)

- 1% fuel surcharge waiver (400 INR to 4000 INR)

- Buy 1 Get 1 Bookmyshow offer has been discontinued from April 2024

My Experience

I’ve been holding the regular Axis Magnus Credit Card ever since it was launched and then moved to the Axis Magnus Burgundy when they initially rolled out the LTF offer.

It’s highly lucrative for sure and have been using it for both domestic & international spends.

The only downside of the card is the long list of exclusions, including utilities, which is quite unacceptable for card of this grade.

Should you get it?

If I look at the recent consultations, I’ve always suggested the Axis Magnus Burgundy Credit Card as a primary card, especially when the annual spends are ~40 Lakhs or more.

If the spends are slightly on lower side and still wish to get better return on spend, multiple Axis Atlas & Amex Platinum Travel Credit Cards in the family would also help.

That said, Atlas Credit Card is quite a lucrative card even now and can as well get devalued further anyday but Magnus for Burgundy might stand bit longer as it’s tied to NRV which gives some profit to the bank.

And not to mention that Axis Bank doesn’t like you to do business spends on their cards.

So, if you’re holding Magnus Burgundy or if you intend to apply for one, make sure to keep an eye on the latest updates which the bank communicates from time to time, so that you’re not up for an unpleasant surprise.

How to Apply?

- Eligibility: 30L NRV to start with; then 30L NRV or 10L AMB

If you already meet the eligibility criteria and hold an existing Axis Bank Credit Card, call Axis Bank support and you should be able to apply over the call.

If you’re new to bank, then you’ll need to follow the 30L NRV route for quick issuance, via branch.

Bottom line

- Cardexpert Rating: 4.8/5

Axis Bank Magnus Burgundy Credit Card is a wonderfully rewarding credit card for high spenders. It’s a must have card for those who’re spending >1.5L a month.

While it’s undoubtedly a great card with no limits on earning capability, capping the Group A redemptions to only 2L a year feels too low, except for Accor Hotels that gives exceptional value.

I wish the bank increases that number or perhaps moves some partners to Group B in future.

If that’s not going to happen, we’ll have to rely on additional cards like Axis Atlas for redemptions beyond 2L Points in a calendar year.

Thanks Sid,

For this Review.

I wanted to check of Government Spends (TDS, Advanced Tax) are considered for annual fee waiver.

if we does swipe directly at school or educational institutes we pay via online link do we still get spends counted for magnus burgundy card?

also will this spends counted towards AEP calculation or normal spends only?

Yes for both.

does education spends give reward points on the axis magnus credit card?

Yes, but they’ll 1%+GST for third-party education payments like Cred, Housing, Phonepe, etc

Card will be downgraded to regular Magnus card(non Magnus Burgundy card) with Airmiles transfer as 5:2 ratio.

If i get this card now, and say after 3 months , bank downgrade my burgandy account due to non maintainence, what would happen to card? Will they close next year?

Is Jewellery / gold spend considered for rewards ?

No rewards for gold or silver purchases as mentioned in their website.

There is a monthly cap of 5K points

Thanks Ramesh . Is there an any document that mentions this cap? I tried reaching out to their customer care but they are either clueless or claim that there is no such cap or limit.

Can anyone suggest if there is any daily/Monthly cap on 5x Edgerewards we get via Grabdeals (for Magnus Burgundy CC) ? I tried getting an answer via customer care and he mentioned “I guess there is no cap”.

Hi you said that you got the Axis Magnus for Burgundy as LTF. I also got this card migrated from Axis Magnus in 2023 September after the major devaluation.

I do not remember it being LTF. Do you have any document to support that claim, because today i called the customer service and they said , my renewal is due on September 2025 and i need to pay 35000/- including GST.

I am having the card against TRV .

It’s LTF for customers maintaining true Burgundy status and LTF offer is removed 3-4 months(around Jan’24) after major devaluation.

Hi Sid/Guys

Can someone help me with an approximate point value for Group B, mainly Qantas, Air India and IHG

Based on my rough calculation for Air India, the best value you can achieve is only INR 0.7 (70 paise), which is relatively low.

I’m struggling to understand where I can use the points after the Group A transfer is utilised.

Air India value more than 1 if used for business class long haul.

Ordinary magnus as well as magnus for burgundy currently earn 12/200 RPs upto 1.5L spend in a month, increasing to 35/200 beyond. However effective 20Jun, spends beyond credit limit + 1.5L will earn 12/200, thus capping the accelerated earning. This will impact big ticket spends such as luxury cars or vacation spends. You could spend from the card, prepay it to free up some limit, again spend more to keep earning 35/200 . That will now get limited.

This is a fair deal and I support banks doing this rather than devalue the whole card for legitimate users.

For people buying cars and other big-ticket items in India, this may still be a viable option, as they can split the payment into two instalments if they plan and purchase such items at the end of the month.

The only people affected are those who are taking an international trip; they will now be at a loss.

I have used my entire card limit and now I want to book air ticket from travel edge portal

So what is eligibility criteria for 60 AEP/200 spend ? Will I get the AEP even if I have consumed my card limit !

Also what is best way to increase card limit ?

You won’t get AEP after consuming more than credit limit. You can try increasing CL via RM.

What is next best redemption after group A limit of 200K transfer point exhaust ?

I need help from the community.

I want to upgrade magnus to magnus burgundy.

I’ve burgundy account, but never maintainer the AQB.

Can I maintain for 1 month and ask them to upgrade?

Thanks in advance!

You need to maintain AQB for 3 consecutive months & then ask for an upgrade, You will need to pay one time 30K+GST & card will be LTF till you maintain AQB. If AQB goes below, they will charge the fees.

Same boat as you. I have added 10 lakhs to my savings account. AMB will be 10 lakhs after 1 month and then I can call customer care and check. Spoke to a credit card agent of Axis bank who told me this

I am trying the same. no luck as yet.

Let me know if you have had any luck

For me edge points remained as, it’s irrespective of how it’s accumulated in the past, but you can reconfirm with customer care.

When you migrated from Magnus to Magnus burgandy – what was the value conversion of the previously accumulated reward points

E.g if you have 2 lac edge reward points accumulated with standard Magnus card (reward point conversion to partner is 80k points) and post upgrade to Magnus Burgundy will my existing reward point become 1.6 lac partner points )?

Great review Sid and as u rightly said this is not for all. Some of us are lucky to get this as LTF and probably without that it may be a challenge. But with LTF I would say blindly that this is the best card in India and no comparison to this.

Hey Sid,

Looks like they’ve increased annual fee waiver to 36L as confirmed by the bank personnel. Can you pls confirm and update?

Any date between 12 and 16 of each month.

Ex: For Jan month, I got AEP on 14-Mar.

After how many days accelerated reward points visible ?

Hi Sid, Thanks for the review.

How to get addon for Magnus Burgundy. I understand they don’t allow that?

Addon card issuance is still on hold, but if you push via branch you may get it.

Do travel edge spends count towards the 1.5 lakh limit for higher reward rates?

No, also Axis Grabdeals not considered under 1.5L spending per month.

Insurnace spends does not generate rewards but will it be useful to cross the 1.5 L / month limit ?

No, insurance transactions excluded from AEP and no base points.

is there any way to track limit on their website weather 1.5 L threshold crossed or not and also for the annual fee waiver.

Unfortunately no options in their website, we need to track in the spreadsheet for each month or calculate manully.

How come infinia is touted as inferior to this card? I have two infinias in family and have been able to use it to extract 16% on flights and 30% on hotels by timing the spend around month end and month start if required. I have magnus as well. but never felt the need to use it as the reward rate is still lower vs infinia. with one infinia one can easily get 1.1lakh flight spend covered per month.

Could someone clarify if magnus gives rewards as said in article for 1. jewellery 2. education when swiping on school machine 3. insurance.

If yes, then magnus beats infinia on above 3. otherwise infinia is still superior. other time magnus could be better when buying a car or so. which I used infina n diner black. but didn’t realise could have used magnus. please clarify on above 3. thanks.

Hi, thank you for a lovely review, I would like to add two points :-

– Annual Spends Capping :- There is a capping on the edge reward points you can consume in a year i.e. you can consume a maximum of 10 Lakh edge reward points in a year ( before the 5:4 conversion ) which means you have to cap your spending at Rs 69 Lakhs a year. = 5.75 Lakhs a month, After this you will only keep accumulating points which you cannot use & Axis may devalue these down the line.

– Amazon Pay vouchers :- The conversion of edge rewards to Amazon pay vouchers is approx 2.8 % as compared to 1.5 % on infinia- this is almost double, which is great.

Summary : The Magnus burgundy is fantastic at more than 10 % ROI ( after 5:4 conversion) compared to my Infinia at only 3.3 %. If your spends are more than 65 Lakhs a year then exhaust MB limit first and after that switch over to Inifinia.

Good summary, but should not one use infinia and exhaust it first, IFF booking flights and hotels on smartby?

Flights -points value you get

Axis Travel Edge – 24%

Inifinia Smartbuy- 16.5%

Hotels – points value you get

Axis Travel Edge – 24%

Inifinia Smartbuy- 33%

For hotels use Inifinia Smartbuy and for flights use Axis Travel Edge

I have the card as LTF basis salary and it’s the best thing there is around.

One optimises all spends, buying of apay vouchers helps to pay off utilities and insurance, bunching spends once in 2-3 months helps hit AEP atleast 4 times a year. Sometimes office reimbursable spends help bump up the ERs

Only downside is getting holiday from work to enjoy the rewards and the capping of Group A

Sid – there is a highly rewarding DC if you understand what I mean. Do you have it ?

No, I don’t have that, neither the Olympus, as I was not into Citi.

Yup Olympus would have been nice given a seperate bigger transfer limit of the accumulated ER.

Would be good to meet up and a few like minded folks.

Cheers Sid.

how do you buy apay vouchers on MB ? gyftr doesnt give any accelerated points on MB AFAIK

Did you get the LTF card recently? I was planning to open a salary account, but they are not giving Magnus LTF. Is there any workaround to get this LTF?

I have this card as LTF, which I got right after the major devaluation.

I honestly think with LTF, it is the best credit card in India, beating even infinia

What happens to the already accumulated points on Magnus to Burgandy conversion. I have approx 2Lac ER points

Will be available at 5:4 post card conversion, as of now. But this can change any moment!

Hey sid, are you aware of how to get the add-on for MB card?

I have Magnus Burgundy and HDFC Infinia both.

For infinia getting add-on was so smooth.

But it’s been impossible for Magnus.

I heard it’s put on pause again. But usually the branch can take some additional approval and get it done from time to time.

hi sid,

great review. I had a question with regards to the accelerated reward points on spends above 150000 is it based on calendar month or statement to statement spends?

It’s based on calendar month.

This card may be good only if spends are very high, higher than ₹ 1.50 lakhs a month, even then for the first ₹ 1.50 lakhs the return will be on the lower side. For moderate spenders, if one can make good use of Smartbuy, infinia would be better. Adding spend requirements for lounge won’t make difference as this card is meant for high spenders anyway. But it doesn’t look nice after a fee of ₹ 30k.

What does this mean – Axis is yet to get strict on the “true” burgundy eligibility

Are there chances that they increase the burgundy threshold requirements?

Meaning, they’re not downgrading/charging the LTF cards even when accounts are not maintaining the burgundy criteria at Cust ID level.

NRV to maintain for card: 30 L , one get max 8% over that which = 2.4 L

if was kept in simple mutual fund minimum 12% = 3.6 L

Difference : 1.2 L

Per annum cost of card : 35,000

total damage: 1.2 + o.35 L = 1.5 L

money needed to be spent to just break even at 10% return from card is 15 Lakh minimum.

If 15 lakh is spent on card with even 3% return than also person get about 50,000 worth of points from other cards.

so to make up for that 50,000 another 5 L needs to be spent on magnus burgundy.

Is it still worth all the effort and what all terms and conditions and this and that?

So till 20 L spends it is just an eyewash card, makes lots of money for bank, taking money from one hand of customer and than giving back from other hand with lots of restrictions, terms and conditions.

People get something from card only beyond 20 Lakhs of spend per year and all this considering that 10% return is there.

If mutual return is even higher that breakeven after shifts to higher value.

If someone gets 4.8% regular return, most of the months, than breakeven is shifted even further to may be 30-40 lakhs.

it is more of marketing gimmick card than being a real banger.

Bank makes money from from FDs, from card fees, spends and commissions from airlines and hotels, and tell you this can not be done, that can not be done. Spend this to get that.

Rating should be 2/5 considering all the above.

30L is only to start with. 10L AMB also works in which case the math is different.

Anyway Axis is yet to get strict on the “true” burgundy eligibility, hopefully they do someday and improve the benefits.

That aside, I think it’s meant for those who are comfortable to move around 30L/10L easily, not for all and so the rating varies with the profile.

Even at 10L AMB , one gets only 40,000 for 1 year at 4%interest although at 12% for MF , it would be 1.2 L. Difference 80,000. Plus 35000 fees. Total damage 1.15L.

Amount to recoup this at even 10% return rate is 12L. Till 12 L return is zero . At 4.8% , breakeven is 25L.

And your 10L are struck, can not use them as well.

Infinia at 25 L gives around 1L return, no questions asked. Not many restrictions.

This card has so convoluted and so many terms and conditions.

And even if you some how earn more than 2 L points even after hooping through all the hoops you can’t use them effectively and efficiently.

At most price points and at most spend levels it is a much poor card compared to even DCB Metal.

They basically take your money, and then tell you how to use it at their terms.

If someone has to anyways do FD only for such large amounts than it’s an exceptional card , otherwise it is truly marvelously packaged deception.

Well summed up Rahul!

If you plans for international trips like costing more than 2 Lakhs then, math goes like below

200k/200 = 100 x 60 = 60000 * 0.8 = 86.4K (Accor)

And you spend in trip month assume 200k then math goes like 25.6K (Accor)

Total = 112K and rest month regular spends on 5x AEP

Keep (financial planning)ur emergency fund in Axis

So your entire trip goes to recover the costs , what you have already paid to axis for M4B. and you have to think and fulfill multiple conditions as well.

If same was spent on Infinia you would be up by more than 30,000.

4L on travel = 15, 000 + 15000 = 30,000

plus if you can time correctly last days of one month and first day of next month = 15000 + 15000+ 10000= 40000

without much fuss and muss.

M4B remains not a good choice for someone with once a year trip or even someone who spends 20-30 lakhs per annum.

remember there are lots of terms and conditions for earning as well burning for M4B.

For it worked like charm. My spend was like 13 lakhs in 4 month. And got 235k points.

So you have assumed that everyone who is using M4B is maintaining 10 AQB. Many people have got LTF M4B based on their salary> 3 LPA. I don’t maintain any balance with Axis, so your entire FD calculation goes off.

Your calculation is based on 12% MF return. That’s not the reality.

It’s not FD it’s MF.

For shortm term like 1-2 yrs, 12% guaranteed return is rare

I think for many this type of rewards will give Luxurious stay in 5 star properties across globe which one does not enjoy without reward points even if capable off .

So Author has given prefect verdict for High Spenders and travel lovers by giving 4.8

NRV includes Mutual Fund holdings so the above comparison is not valid

for demat holdings NVR is 1 crore, basically again you are paying 1% more = Rs 1 Lakh , as fund management fees to axis over the direct mutual funds.

one can calculated anyways, axis is going to charge you almost same money all the ways, that’s how they are funding the entire program.

How to get the guest access for lounge using this card?

As they are not allowing to get add on cards for Magnus Burgundy.

Just use the card or priority pass directly with guest as +1 or as required.

Thanks for the much awaited review of Magnus burgundy. Very well summarised and crispy review as always. Can you let me know regarding accelerated points using gyftr and grabdeals? I was planning to get this card for buying a car. What do you suggest. Thanks